The 2020 condo market in Boston was characterized by unusual patterns of inventory and sales transactions as compared to previous years. The Spring market was interrupted by initial covid lockdowns, buyers and renters left the city to work remotely, and inventory ebbed and flowed in atypical form.

Sales Transactions

Condo sales transactions were down -13% in 2020 compared to 2019 (off by a total of 379 transactions). It was the lowest number of sales transactions since 2011. While often a dip in sales year to year signals a significant new construction building(s) closing the prior year, in 2020 the new construction closings were only down by 20 units. For 2020, the loss in transactions was simply due to market conditions created by national and global events.

Comparison of New Construction Closings 2020 vs. 2019

Echelon

Pier 4

One Dalton

Total:

142

9

39

190

36

95

79

210

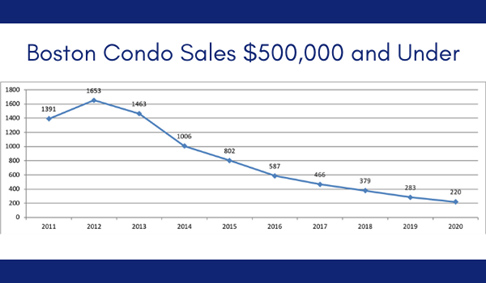

Sales activity varied segment to segment. $500,000 and under sales were off -22% but this is a segment that has been disappearing over the last 10 years. In fact, the $500,000 and under sales have been tracking at a 20-30% reduction each year for the last 10 years, so this past year’s -22% reduction was not unusual.

Sales $1.5M – $1.99M were up +5% in 2020 compared to 2019, while sales $1M- $1.49M were down -11% and sales $2 – $2.5M were down -15%. Several factors contributed to a lag in luxury sales in 2020:

• Many luxury buyers fled to the suburbs to wait out the pandemic in single family homes, driving the single family home market into a frenzy of bidding wars and a surge in prices. (For example, in Hingham the average days to offer decreased by -20% and the average sale price increased +14% from 2019 to 2020).

• Remote work and school encouraged many luxury apartment residents to take a break from city living and instead rent a beach house, lake house, mountain home, etc. leaving an unprecedented apartment vacancy rate. For those committed to city living, incredible opportunities awaited in fully amenitized new apartment buildings to sway would-be buyers to become renters as they wait out the uncertainty of the global virus crisis and a turbulent election period.

• Inventory was unbalanced all year as sellers tried to determine whether to list or not and when to list. In addition, many condo buildings prohibited showings and open houses for the first half of the year as condo boards and management companies tried to understand the risks and liabilities of the covid-19 virus. The Spring market inventory was down by over -20% compared to Spring 2019, but by Summer 2020 the inventory was up over +60% compared to Summer 2019. The large swings in the market inventory led to confusion and uncertainty for buyers and sellers.

Neighborhoods that were able to offer lower priced inventory in low rise buildings fared better through 2020. For example, the North End saw a 41% increase in condo sales and a 3% increase in the average sale price in 2020 compared to 2019. Much of that inventory was older stock condos that were commodity rental product. As investors tired of sitting on vacant rental units unsure of when schools and offices would reopen, they began to list their units. Charlestown also experienced a small -1% reduction in sales and a 6% increase in the average sale price.

The biggest gap in 2020 sales was in the high-end segments as ultra high net worth buyers retreated to their other homes and put off buying for the year, and international and out-of-state buyers faced travel restrictions. As a result:

- $2.5M – $3M sales were off -30%

- $3M and up sales were off -41%

- $4M – $5M sales were off -55%

Pockets of Strong Activity

In spite of a slower year for transactions, there were still areas of urgency and momentum. For example, in the $2M- $2.5M there were still 27 units in this price range selling in less than 30 days and there were 8 units that sold at or above asking price. These units in top demand were spread out across the various neighborhoods, with sales recorded in Back Bay, Beacon Hill, Charlestown, Fenway, Midtown, South Boston, South End, and the Waterfront. What they did have in common, however, was outdoor space. Of the 27 units that sold in less than 30 days, 22 had private outdoor space, 2 had common area outdoor space, and only 3 had no outdoor space (though all of these three were yards away from significant public park space).

And while $1M+ were down -15% overall year over year, there were pockets of steady activity. The South End only fell short of its 2019 sales number by 2 units. Beacon Hill only missed its 2019 $1M+ sales mark by 7 units. Other neighborhoods such as Seaport, South Boston, Waterfront, and Back Bay saw much larger reductions in $1M sales (as well as sales overall).

Sale Prices

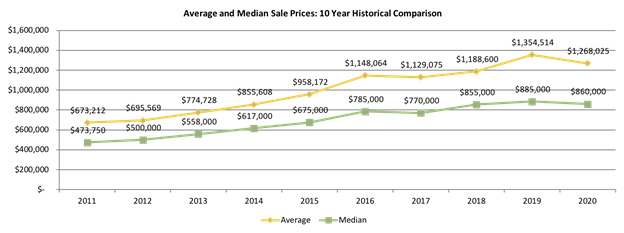

Overall, average prices declined in 2020, dropping roughly -6% below the 2019 average due in large part to the reduction of sales in the ultraluxury price segments. Still, Boston fared better in 2020 than may have been perceived. The average price was still the second highest recorded for the last ten years. Only 2019 had a higher average sale price and that was mostly a result of the first round of closings for Pier 4 and One Dalton.

For more detailed analysis of the 202 Boston condo market and the forecast for 2021, contact RESIS.

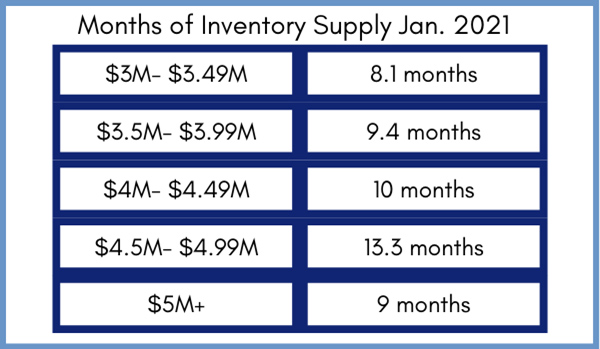

Meanwhile, $2M – $3M inventory remains balanced between buyers and sellers at approximately 5 months of supply. Inventory under $2M, however, is still tight. $1M – $2M is below 3 months of supply, and supply levels drop to just 2 months of supply under $1M. Although under $1M inventory is tight, there is more opportunity for buyers in this segment right now than in years passed (inventory was even tighter over the last few years, hovering around a one month’s supply).